$3,500,000 Refinance in Tracy, CA

$3,500,000 Cash Out Working Capital Loan

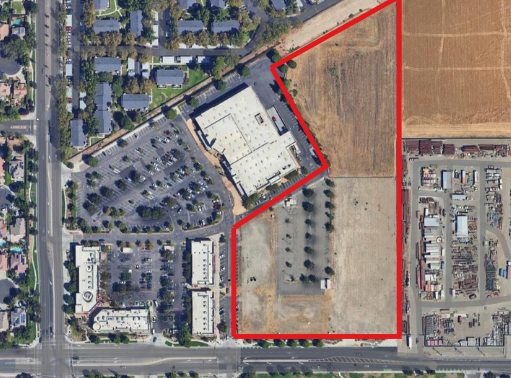

on a 9.5-Acre Portfolio

Loan Amount: $3,500,000

Loan Term: 12 Months

CLTV: Under 50%

Lien Position: 1st Deed of Trust

How we funded a complex three-parcel refinance, brokered to us by a fellow private lender who needed a capital partner.

The Opportunity: A Cash Out Working Capital Refinance

When an experienced investor needs liquidity fast, a cash out working capital loan backed by real estate equity is often the most efficient tool available. This deal is a prime example, a $3,500,000 refinance in Tracy, California, structured to pull working capital from a high-equity portfolio without requiring a sale or traditional bank timeline.

The collateral consisted of five total assets: three individual parcels and two non-owner-occupied single-family residences, spanning 9.5 acres in total. The combined loan-to-value came in well under 50% CLTV, providing a strong equity cushion from day one.

The Deal Structure

Three Individual Parcels: Zoning Play in Motion

The borrower originally paid $5,100,000 cash for three commercial lots adjacent to a retail center in Tracy. A family-connected realtor identified an opportunity: the parcels could be re-entitled from commercial to residential zoning, allowing the land to be repositioned for townhome-style development. Once the entitlement is secured, the plan is to sell the entitled lots to a builder, converting raw commercial land into a premium residential development site. This type of value-add land strategy is exactly where a short-term, 12-month bridge loan makes sense.

Two SFR Properties as Supporting Collateral

In addition to the three parcels, the borrower pledged two non-owner-occupied single-family residences to further strengthen the collateral package. This cross-collateralization gave us added security and helped keep the CLTV comfortably under 50%, even at a $3.5M loan amount.

Why We Were Comfortable Funding This Loan

Before committing to a deal of this size, we reviewed the borrower’s full portfolio. What we found was an investor with substantial assets, a track record of executing complex transactions, and a clear, well-defined exit strategy. This is the type of experienced borrower profile that makes a large cash out working capital loan straightforward to underwrite: strong collateral, low leverage, and a credible plan.

Key underwriting factors: Sub-50% CLTV across the full collateral pool, substantial borrower net worth, proven execution history, clear exit via entitlement and parcel sale to a builder, and a 12-month term aligned with the re-zoning timeline.

Working with Other Private Lenders

This deal came to us through a fellow private lender who had identified the borrower but couldn’t fund the full $3,500,000 loan on their own. It simply exceeded their available capital. Rather than walk away from a quality deal, they brokered it to us.

We actively welcome these co-lending and broker relationships. If you’re a private lender or mortgage broker sitting on a deal that’s too large, too complex, or outside your usual box, bring it to us. We have the capital, the underwriting experience, and the flexibility to move quickly on large loans that require a real decision-maker, not a committee.

The Bottom Line

A well-structured cash out working capital loan gives investors the liquidity to fund operations, acquire new assets, or carry a repositioning play, all without selling the underlying property. This Tracy transaction checks every box: low leverage, experienced borrower, strong collateral, and a clear path to payoff. If you have a similar deal, we want to hear about it.

Need a Cash Out Working Capital Loan?

We fund complex, large-balance private money loans across California. Reach out today to discuss your deal.

To see more funded deals, click here!

To keep up with us, click here!